August 28, 2025 — Nvidia, the world’s most valuable semiconductor company, reported another quarter of record-breaking revenue on Wednesday, yet its shares slipped in extended trading as investors weighed signs of slowing growth and fresh concerns over its China business.

The stock fell 3.14% to $181.60 in after-hours trade, erasing nearly $110 billion in market value and reducing the company’s market capitalization to $4.43 trillion.

Q2 Results Revenue But Growth Moderates

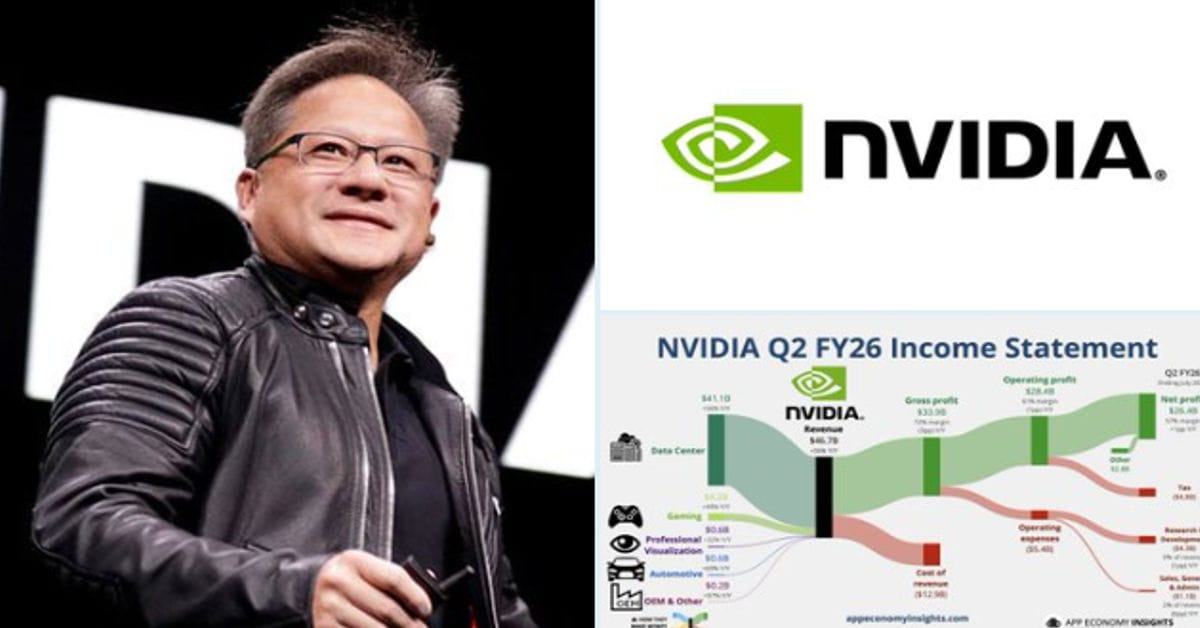

For the fiscal second quarter ended July 27, Nvidia posted revenue of $46.7 billion, up 56% from the same period last year and slightly ahead of Wall Street’s estimate of $46.2 billion.

While the topline number marked yet another record for the chipmaker, it also represented the slowest pace of growth in more than two years, sparking investor concerns that the explosive demand for its artificial intelligence (AI) chips may be stabilizing.

Nvidia’s adjusted profit came in at $26.4 billion, or $1.05 per share, comfortably beating the consensus forecast of $1.01 per share.

Segment Performance: Data Centers Still Dominate

Breaking down its revenue, Nvidia’s data center business remained the primary driver, delivering $41.1 billion in sales. This figure, however, came in slightly below analyst expectations of $41.3 billion, suggesting some cooling in what has been the company’s most lucrative division.

The gaming unit provided a bright spot, generating $4.29 billion in revenue and exceeding forecasts of $3.8 billion. Nvidia’s graphics processing units (GPUs) continue to find strong demand among PC gamers and esports enthusiasts, bolstered by new product launches.

Meanwhile, the automotive segment contributed $586 million, narrowly missing projections but reflecting steady momentum as Nvidia expands its footprint in autonomous driving and in-car computing systems.

Aggressive Stock Buyback

In a move aimed at rewarding shareholders, Nvidia’s board approved a new $60 billion stock repurchase program, one of the largest in corporate history. This is in addition to the $14.7 billion that remained under its previous buyback plan at the end of the second quarter.

The move underscores management’s confidence in the company’s long-term prospects, though critics argue that such massive repurchases may do little to address near-term growth challenges.

Q3 Outlook: Strong Guidance

Looking ahead, Nvidia issued upbeat guidance for the third quarter. The company expects revenue of $54 billion, plus or minus 2%, compared with analysts’ average forecast of $53.14 billion, according to LSEG data.

This outlook suggests continued momentum in AI chip demand, particularly from cloud service providers and enterprise customers investing heavily in generative AI infrastructure.

Despite the strong results and positive forecast, concerns over Nvidia’s China business weighed heavily on investor sentiment.

READ ALSO – Actor Rajesh Keshav on Life Support After Collapse at Kochi Live Event

The company disclosed a $4 billion decline in sales of its H20 processors, chips specifically tailored for the Chinese market. The decline comes amid escalating US-China trade tensions and restrictions imposed by Washington on the export of advanced semiconductors to Beijing.

Crucially, Nvidia’s third-quarter guidance excludes any contribution from H20 sales, underscoring the uncertainty surrounding its operations in the world’s second-largest economy.

Waiting on Washington’s Approval

Chief Executive Jensen Huang addressed the situation, saying Nvidia expects to resume shipments of H20 processors to China once it secures US government approval under a deal reportedly negotiated with President Donald Trump.

The arrangement would involve Nvidia paying commissions to Washington in exchange for limited approval to sell its processors in China. However, the framework remains uncertain, with no formal rules in place and the risk of potential pushback from Chinese regulators looming large.

Until clarity emerges, Nvidia has opted to exclude China-related revenues from its near-term financial outlook. Analysts warn that prolonged delays could impact the company’s market share in China, where rivals may attempt to fill the gap.

Investor Sentiment: Balancing Optimism with Caution

Market watchers noted that the post-earnings dip in Nvidia’s stock reflects a mix of profit-taking after a massive rally and genuine concerns about sustainability. Over the past two years, Nvidia’s shares have surged on unprecedented demand for AI chips, making it the fourth-largest company in the world by market value.

“The market is asking whether Nvidia can keep growing at this pace, especially with macroeconomic risks, regulatory hurdles, and competition in AI hardware intensifying,” said one analyst.

Still, others remain bullish, pointing to Nvidia’s dominant position in AI computing, its massive cash reserves, and its shareholder-friendly policies like the new buyback.

ALSO READ- Bigg Boss 19: Gaurav Khanna Reveals Wife Akanksha Chamola Doesn’t Want Kids

For now, Nvidia continues to deliver record revenues, but the combination of slowing growth, geopolitical risks, and sky-high expectations has tempered investor enthusiasm.

The company’s third-quarter performance, particularly its ability to navigate the regulatory landscape in China while meeting robust global AI demand, will be closely watched by Wall Street.

As Nvidia navigates this pivotal moment, the question remains: can the chip giant sustain its meteoric rise, or will external challenges begin to chip away at its momentum?